Greater Phoenix Income is Rising

The Summer Season is Upon Us

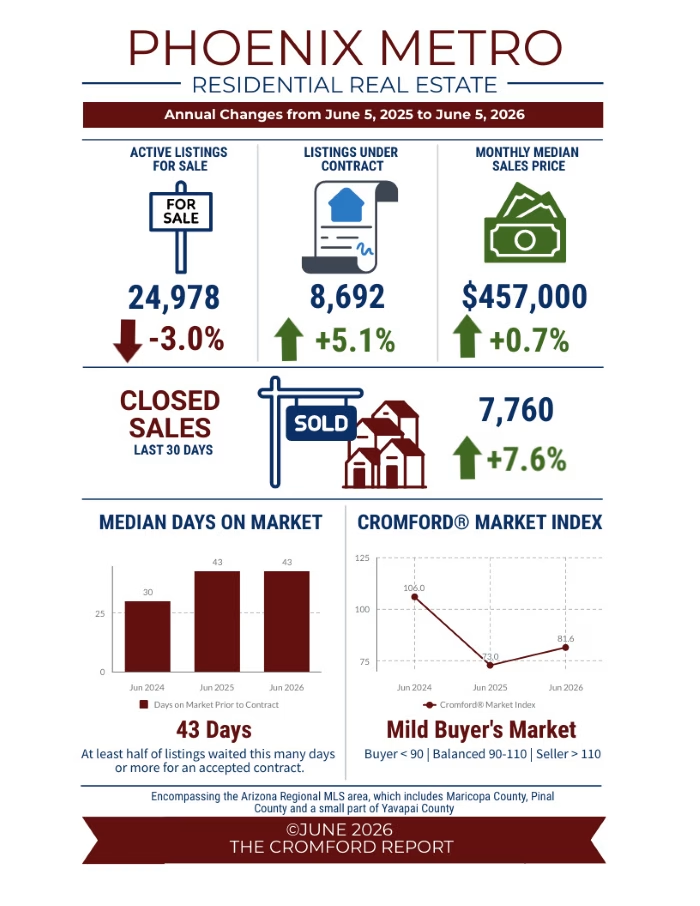

For Buyers

Incomes have been continuing to rise in our state. According to the most recent release from the Bureau of Economic Analysis, Arizona ranked 7th in the nation for nominal personal income growth at 4.3% and Arizona’s net earnings from work rose 5.7%. Both measures are well above the rate of inflation. Combined with home values remaining nearly unchanged year-over-year and mortgage rates holding near 6.6% over the past month, this suggests housing affordability is gradually improving.

Home values have been mostly flat for the past two years, and the median is still down 4.8% from the peak price of $480,000 recorded June 2022. However, homes below $500K have drifted down 4-5% during the same time frame, while those between $500-$1M have remained stable with little fluctuation. Meanwhile, homes over $1M surpassed 2022 a long time ago and are still on the rise in value.

The past 4.5 years have included a sharp price spike in 2021, followed by a correction in 2022 and very little appreciation from 2024 through 2026 for most homeowners. However, the likelihood that the next 5 years will follow the same trend is low. Purchasing in a buyer’s market is usually best for those who plan to own their home for at least 5 years in order to ride out cycles like this one, which turned towards a buyer’s advantage in November 2024.

There are advantages and disadvantages for buyers in today’s market. A major advantage is a lack of the frantic buyer urgency that was experienced in 2021, fueled by low supply and rapid population growth. Back then, buyers often only had a few minutes to tour a home, then felt pressured to waive appraisal and inspection contingencies as multiple offers flowed in. Asking for repairs was out of the question and 61% of sales were over asking price. Today, most homes are on the market for more than a month before landing a contract. Reduced buyer competition has made negotiations less stressful for buyers and increased seller willingness to offer repairs and closing-cost assistance. This can include a temporary mortgage rate buydown and cost the seller about $10,000. This level of seller aid was unheard of prior to 2023.

The disadvantage to buying in today’s buyer’s market is that home values tend to have low appreciation, no appreciation, or negative appreciation. Buyers typically like to purchase a home and watch it appreciate in value, but buyer’s markets can put a homeowner’s patience to the test. Those who purchase in this market should generally expect to own the home for at least 3-5 years to ride out the cycle. During that time, if a homeowner significantly improves the property it will improve their chances of building equity sooner.

While appreciation has been limited recently, buyers who hold their homes through a full market cycle can still build substantial wealth through a combination of appreciation and mortgage principal reduction. If the housing market pulls out of its slump over the next 5 years to average a mild 3% appreciation per year, a buyer who bought a median-priced home around $450,000 with 10% down could build equity faster than they might expect. After 5 years of just appreciating around the rate of inflation, there would be over $72,000 in appreciation, plus another $25,500 in equity from making the principal payments. Including the original down payment, that would amount to approximately $142,500 in total equity while enjoying the benefits of homeownership. This is why homeownership is often referred to as a “forced savings account”.

For Sellers

Buyer demand is up despite higher mortgage rates as listings under contract are up 5.1% and closed sales are up 7.6%. This year’s buyer’s market, while not ideal, is an improvement over last year. There is evidence of pent up demand that is often revealed once mortgage rates push below 6.5% and increases when it’s closer to 6.0%.

However, Greater Phoenix is now entering into its summer season. This comes with hotter weather, and a few holiday speed bumps starting with Memorial Day week. Whenever there is a 4-day work week buyer contract activity takes a dip, and this Memorial Day was no different, dropping 21% over the course of 2 weeks. Then, just as activity begins to recover, the market encounters the Fourth of July holiday week, followed by Labor Day.

Many sellers have decided to wait it out. New listings are added at the 2nd lowest rate seen since 2000, the fewest new listings were added in 2023 and 2026 looks like it will be in second place. Meanwhile, cancelled listings are up seasonally, but down year-over-year, which is also contributing to a decline in supply.

What to watch: Last year mortgage rates fell from 6.6% to 6.1% from August to September. That resulted in a spike of buyer contracts until Labor Day week hit and contract activity cooled. If that happens again this summer, sellers could see a better boost in buyer demand.

Commentary written by Tina Tamboer, Senior Housing Analyst with The Cromford Report

(c)2026 Cromford Associates LLC and Tamboer Consulting LLC